Decentralized Conglomerates #101

Sharing a few essays by David Landry and my thoughts on decentralized conglomerates

The power of decentralized capital allocation (specifically M&A) continues to receive more attention as conglomerates/holdcos show continued success in their ability to effectively deploy capital.

Working at Constellation, the fact that operators aren’t held back from making their own acquisitions/capital decisions (strategic or non-strategic) appears to be quite freeing. As long as an investment can be justified and projected results are reasonable, you're free to go ahead and deploy capital. The collective number of deal reps allow operators and M&A teams to become disciplined investors fairly quickly.

In a more centralized world, operators would need to go through the dreaded capital planning process, where they put together their wishlist, send it up the chain, and hope that the prioritized list includes their initiatives. Once receiving approval, there's a massive push to spend capital right away as situations can change at any moment and the capital available could quickly disappear. This often leads to poor cost management (e.g. overruns, unrealistic timelines, bloated budgets) and ultimately lower returns.

When it comes to acquisitions, the lack of familiarity with M&A (deal sourcing, structuring) along with internal support (tax, legal) makes it too much work to actually get a deal done. This is especially true for smaller deals as they rarely move the needle (relative to the effort involved). Moreover, the lack of deal reps often leaves a gap between the planned M&A process and what ends up happening.

When it comes to studying conglomerates and the power of decentralization, David Landry (Portfolio Manager at Demesne Investments) has written a number of essays that have been quite helpful in building my personal thinking.

You can check it out on his newly created website here. Some of my favorite essays include:

Below, I’ve included some takeaways from David’s essays along with a few of my own thoughts. However, I'd strongly recommend reading these essays if you're interested in the topic.

Practice Makes Perfect

This is an interesting essay that compares the approach of two serial acquirers - Constellation Software and J2 Global. It introduces the category of 'programmatic acquirers' and the success that comes from doing multiple smaller deals.

The case for programmatic acquirers is summarized by David below:

Smaller companies tend to be cheaper than larger ones

Smaller acquisitions tend to be of lower risk to the acquirer, by virtue of relative size and simplicity

Private companies tend to be cheaper than larger ones

Repetition (in acquisitions) builds skill.

With the abundance of capital in the market today, I'd say that the first point continues to be challenged (to the benefit of founders/operators). It is no secret that valuations for stable and predictably cash flowing businesses (regardless of industry) have never been quite as high as it is today.

With that said, I do believe that our definitions of market/company size and the associated risk/reward of buying businesses need to be continuously revisited. For example, the definition of a ‘small’ business and the risk associated with acquiring it doesn’t appear to be the same as it was a couple of years ago.

The 1960s Conglomerates Boom

This essay was a great history lesson on what went wrong and right during the 1960s Conglomerates Boom. The line that caught my attention was the following: "I do not think the Conglomerate Boom condemns the conglomerate model, but it does show us how not to build them: with ever-larger acquisitions, leverage and entirely unrelated diversification."

When I think about the acquisitions taking place today, we're seeing investors (strategic and especially financial) pursuing large and small acquisitions with a considerably high amount of leverage. However, we haven't seen conglomerates, in the traditional sense, pursue unrelated diversification. In some cases, organizations have been able to pursue unrelated diversification via organic growth (e.g. Amazon).

The interesting piece that we are starting to see is a next-gen conglomerate that isn't necessarily tied to one holdco but related to one financial investor.

Marc Andreessen describes this concept as he explains the future of a16z on Invest like the Best (as HP 2.0). Here's the excerpt:

"Can we construct in the context of a venture capital firm that is a minority investment and impact companies, can we construct the modern equivalent of what would have been that HP central office from like 1960, and provide our companies with that kind of overlay capability, with all of that reinforcement and brand and help and power that you would have had as a division of HP? But then of course it's a different deal. We're not in control. HP was in control of all his divisions. We're a minority investor, right? So we ride along with the founder.

So it's a different kind of relationship. They don't work for us, but with the huge advantage that we have no need for strategic consistency. We're not an operating company. And so as a consequence, we are completely unbounded in terms of how many different sectors we can invest in. We're completely unbounded in terms of how many different companies we can invest in, assuming we can find quality companies.

I'll just give you an example. We now have 250 companies active in the portfolio today where we own more than 10% of the company. HP or IBM at the peak of their power, they didn't have 250 divisions. They didn't have anywhere close to 250 divisions. There is a scalability in the venture model that in theory is much broader. We can provide a much bigger umbrella across all these companies, with the trade off that we don't have majority ownership. We have minority ownership, and we don't have control."

Now apply this idea to any of the large PE funds and you'll see that they share a number of characteristics with decentralized conglomerates. Portfolio companies often share best practices, receive management support and have access to support functions (e.g. legal, tax, M&A and etc).

As their capital pool grows, a financial investor can build specialized (or diversified) platforms to the point where they can essentially behave like a decentralized conglomerate.

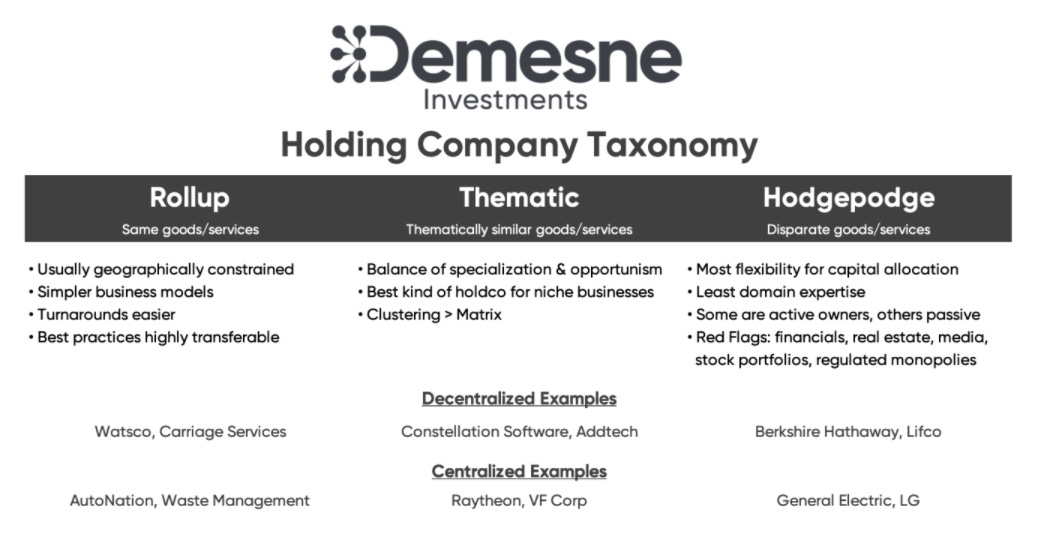

Taxonomy of Holdcos

This was an interesting essay that presents how to categorize conglomerates, which was an area that I was personally struggling with. It is summarized quite well in the table below:

As pointed out above, there is no 'right way' to build a holdco as there are successful examples across the board. While the optimal goal may appear to be the thematic holding company, it takes a fairly strong culture of discipline to strike the balance of specialization and opportunism. The larger the holdco gets, the easier it is to either be stuck in their ways and opt to specialize or make risky bets and expand into unrelated markets. The way to avoid this is to experiment with new ideas within the periphery of the holdco’s core competence where possible.

You'll notice that many PE funds today opt for the rollup strategy - with the ability to buy multiple smaller businesses at strategic valuations (after having an initial platform in place). The interesting revelation to me is that the larger fund itself can function as a passive hodgepodge with investments in a number of unrelated markets.