Fundamentals for Private Deals; First Republic Bank; Wonders of Web3 #115

Fundamentals for Private Deals; First Republic Bank; Wonders of Web3 #115

Reflecting on a few interesting reads and listens over the past week

Fundamentals for Private Deals

This is a great podcast featuring Trey Lockerbie and Brent Beshore, who is the founder/CEO of Permanent Equity. I've always tried to stay on top of his essays/podcasts as they provide a lot of guidance on making investments in the lower mid-market space. I'd highly recommend checking out some of his essays (e.g. the one around compensation) and annual letters.

Brent does a clever job of appealing to his typical acquisition target by always emphasizing his background as an entrepreneur who started a couple of businesses, which accidentally led to buying a business. As someone who interacts with owners/operators of businesses, this is a story that's far more likely to appeal to potential targets than someone who comes from a management/financial background without any 'real operational experience.'

Over the course of the podcast, Brent shares a number of interesting tidbits that were worth sharing.

Making Asymmetric Bets

"I think that the way he thought through deals and the way that we think through them is very similar, which is, what is the downside risk? And then, what’s the upside? And we want to get into asymmetric bets. We want to get into things that if things go poorly, we lose a little bit of money, and if things go well, we can hold them for a very long time and make a lot."

The best investors often try to understand the different scenarios associated with any investment (what can go wrong? and what can go right?) and do everything possible to minimize their downside risk. As you evaluate more deals, you end up building an understanding of what an asymmetric bet often looks like.

Price is My Due Diligence

(Brent recounting his conversation with Warren Buffet and questioning him on how deals were done in the early days) “You give in this air that you meet the guy, and you ham it up, and then you give him a price.” And he says, “Yes, and you shake hands and you write him a check, easy peasy.”

I said, “Come on, you’ve got to diligence these companies. You’ve got to understand what’s going on, and you’ve got to get comfortable with what you’re actually buying.” And he kind of hemmed and hawed in his Buffett way, worked around the edges. And I kept pushing him, kept pushing him, and kept pushing him. And I think he got a little annoyed with me, which by the way, the best sound bites apparently come from getting annoyed with me, because he said, “Price is my due diligence.” That was the hammer that fell on that line of question. And I just sat back and I said, “Well, it makes a lot of sense.” Everyone at the table was like, “Now, what does price mean? How low can you go? And what’s the margin of safety in that?” That’s the art of it.

But it’s true. And it’s something that that quote and that line of thinking have really impacted what we do as well because you can diligence to deal with death. It’s super easy to try to kick over every rock, and that’s not helpful. And I think that depending on the price you buy at and the situation you’re buying into, I think there is a lot of safety in price. And so we try to be thoughtful about that. Of course, in these markets and with the competition that’s out there, price is often a pretty charged issue. So we try to stay disciplined.

Completing diligence for private deals, in some respects, can be more difficult than larger/public companies. The systems/processes aren't in place to run a standardized diligence process and you often need to work with the seller to get the information you need. This obviously can be a source of frustration to the seller who is looking to complete the purchase process as quickly as possible. At some point in the process, both sides will need to develop a sense of trust and focus on areas that are important. From a buyer's perspective, some of this trust is inevitably built into the purchase price. The lower the price/higher the margin of safety, the more risk you can tolerate.

Building a Talent Network

Finding talent, discerning talent is really, really difficult. Oftentimes these businesses get in a situation where they can’t pay to attract top talent and so they settle for inferior talent that they can’t do much with. And so oftentimes we’re coming in again and just trying to help solve a lot of these issues.

We’ve got a talent network called the Orbit, which has been fantastic. We recruit out of it all the time. And these are just people up and down, the seniority law levels, all around the country, and even beyond the United States that are just raising their hand saying, “Hey, would love to come work with you someday. Let me know when something fits my skillset.” And so we’re often calling people sort of the bench, often calling people out of the bench, and works out great for them, works out great for us.

Personally, I wonder whether recruitment is a function that should be centralized within consolidators/serial acquirers (similar to what Brent has done with Orbit/Permanent Equity). On one hand, operators are far more likely to have a better understanding of what the business needs from a skills/experience perspective. However, one can also argue that the quality of people is far more likely to degrade as the 1000th business is less likely to have an understanding of Constellation's model vs. the first business. There's also an opportunity to aggregate the collective network within Constellation to attract a broader range of talent.

First Republic Bank

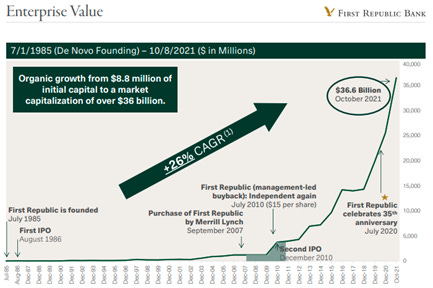

I enjoy reading about compounders and how companies are able to consistently generate outstanding growth/returns. This week I came across this post by Enlightened Capital on First Republic Bank ($FRC). Their track record is quite incredible (see chart below) and stems from a common-sense approach toward banking. Their ability to continuously grow at a high clip and achieve a customer attrition of 2% with a relatively small branch network (80 branches) is quite unique. It appears as though their focus on developing relationship managers and incentivizing them in a way that forces them to pay attention to their existing clients (vs. adding new customers) is a big growth driver.

The Wonders of Web3

Over the past few months, I've increasingly become outdated when it comes to understanding what's going on in the world of crypto (now Web3). For those of you looking to learn more about the current state of Web3/crypto, this podcast by Tim Ferris, Chris Dixon and Naval Ravikant is a great foundational resource. I'd recommend listening to this in chunks and perhaps reading the transcript for reinforcement as well.

While I won't attempt to summarize the podcast, here are a few concepts that I was able to pick up on:

What is Web3? It’s an internet owned by users and builders orchestrated with tokens. This new concept of a token is the kind of the key concept of Web3. This comes sort of historically, from the movement that started with Bitcoin.

Under Web3, we're likely to live in a world where data is secured on the blockchain that is owned and used by its contributors (vs. a select group of corporations as is the case in previous eras).

Why is this important? You can now build something that looks and feels like Facebook or Twitter using open protocols and using this new kind of philosophy where the value and control accrue to the users of the network, not to a company.

How do you attribute value? Tokens are self-marketing. When somebody owns something and feels skin in the game, they want to go talk about it. They want to evangelize it. As this cycle takes place, winning products will become the most valuable tokens. The goal ultimately comes down to maximizing distribution.

What is a NFT? It's too simplistic to call it a digital object. It can take many shapes/forms (pointer, channel, form of communication). Chris Dixon describes it as a web page - which seems like the best way to describe the various possibilities. It can be recognition and reputation. It can be royalties, it can be copyrights. The variability comes from the fact that it's programmable.

Digital private keys enable digital private property, which inevitably creates digital scarcity. This is probably the best way to think about NFTs - you're able to own a piece of the internet.

The idea that NFTs is merely digital art is likely as inaccurate as saying a website/web page is simply a URL (which is ironically what happened in the dot-com bubble).

What do we mean by composablility? This is quite similar to how we think about coding. Instead of having to rebuild functions that have been built in the past, developers have access to a global library that can be copied and tweaked for your own use (Naval makes the reference of taking an existing set of legos and building on top of it).

What does Skeumorphic mean? It's a concept in design of taking something from the offline world, and using that design in the online world to make it look more familiar. Revolutionary products are often not skeumorphic and therefore much harder to identify until users start seeing value from it.