Roll Up to Win #92

A quick look into Canada's latest roll-up - DentalCorp ($DNTL)

For my Canadian readers, I hope you'll appreciate the reference.

During a conversation with a friend this weekend, I was trying to figure out an investment category that Canada really excels at (PE, VC, public, real estate and etc).

The best answer that came to my mind was roll-ups - or to define a bit more broadly the idea of growing via acquisition.

The most recent Canadian success story to IPO here is Dentalcorp - founded in 2011 and has grown to over 412 practices today and just raised over $950M this month (largest IPO on the TSX this year). Prior to going public, Dentalcorp was backed by the likes of Imperial Capital, L Catterton, and OPTrust.

Going through their prospectus, their story is quite similar to other consolidation plays and calls our the following elements. Having seen a number of memos on consolidation plays. They usually consist of:

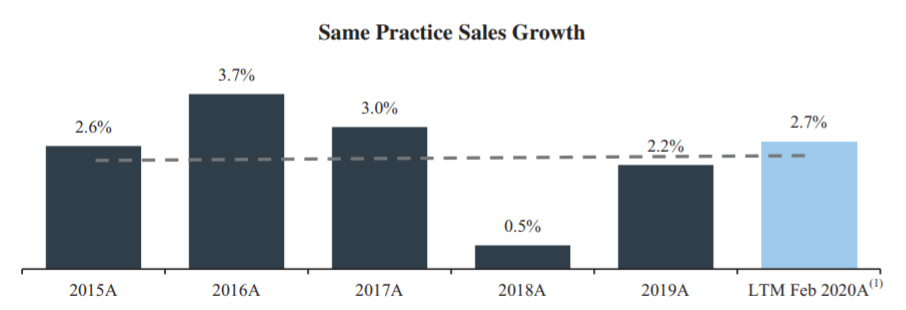

History of Recurring Revenues

Large and Fragmented Market

Repeatable Acquisition Program

Playbook for Driving Organic Growth

History of Stable, Recurring Revenue*

*Not accounting for potential pandemics that can close down most dental clinics.

Large, Fragmented Market

Repeatable Acquisition Program

"Our robust acquisition pipeline positions us favorably to execute on our strategy. We have an extensive and proprietary database of dental practice owners across Canada, and our current pipeline of opportunities at various stages of sourcing and negotiation includes over 500 opportunities, over 100 of which are in more advanced stages of negotiation. Over 14,500 practices exist in Canada which remain independently owned, presenting ample white space for our continued pursuit of double-digit annual growth. Our national business development team leverages strong industry relationships and our reputation within the dental industry to identify new practices for our network on an ongoing basis. We have acquired average annual Practice-Level EBITDA of approximately $41 million during 2018 to 13 2019 and approximately $35 million over the past three most recent financial years (which period includes the COVID-19 pandemic), respectively, while selectively targeting established practices with proven operating track records and strong business fundamentals.

When evaluating a potential acquisition, we target a 15% or greater ROIC."

Playbook for Organic Growth

leading to...

My Thoughts

Overall, DentalCorp appears to be a fairly well-run business - with a lot of opportunities to grow geographically and into other vertical markets. Moreover, if they continue to deploy capital at 15% or above, they'll be able to generate stable returns that are above what most investors will be able to deploy at.

With that said, it overlooks a fairly important part of the story - patient retention/attrition. The fact that the industry norm is to see ~20-25% of turnover within the patient base is a bit concerning as practices may ultimately have to spend more to acquire/retain customers. Personally, I feel as though the switching costs are quite low for basic dental services and are more of a function of convenience (especially when the costs are largely covered by an insurance provider).

This speaks to a larger observation I've seen with potential market consolidation plays. As recurring revenue streams (primarily among software companies) achieve incredibly high valuations, there has been a number of businesses that have re-positioned their businesses to have 'recurring revenues.' This was inevitable and in some cases, may not be a false narrative.

However, a lot of these businesses tend to have recurring customers with fluctuating revenue streams (e.g. payment varies and is not predictable over time). The risk/reward associated with that type of revenue should be valued differently than the traditional SaaS revenue stream. As an investor (public/private), it's important to keep this in mind when you're looking at presentations that are looking to push the recurring revenue narrative.

The Bull Case for Ethereum

For those of you interested in understanding the case for Ethereum, here's a great essay by Packy. I've previously referenced how Balaji recommends that holding 50% bitcoin and 50% ethereum is a very solid way to generate wealth in the next 10+ years. While it might be a bit scary to shift your entire wealth to crypto, it's not a bad idea to have a 50/50 split between Bitcoin and Ethereum within your crypto allocation.

Boyd another great Canadian rollup.

Incredible post. Pushing to do this with GrowthGenius, would love to get your thoughts down the road.