Tiger Global; Excess of Excesses #117

Tiger Global; Excess of Excesses #117

Reflecting on a few interesting reads and listens over the past week

Tiger Global

I really enjoyed this post by Mario Gabriele (author of the Generalist) on Tiger Global. They have recently made a lot of noise in the market due to their unique approach toward VC investing - deploying capital at a slightly lower rate of return at a much faster pace. This has made it difficult for more traditional VC investors who are used to having more time to diligence their investments and not having to run into the challenge of competing purely on price.

Mario goes into the history of Tiger Global - starting from Julian Robertson (founder of Tiger Management) and his influence on Chase Coleman. He then goes into Chase Coleman's thesis in the tech space and what made it so successful. Finally, he wraps up with why Tiger wins in today's market.

Here are a few key highlights that I took away:

Julian Robertson's success can be boiled own into the following:

A gift for spotting talent

A meritocratic approach

Superior pattern recognition

A flexible investing mandate

These are all characteristics that seem easy to have/execute on paper but much harder in practice. More so than any other field/function, I find that a leadership role in investing is heavily weighted on picking the right talent and incentivizing them accordingly. The work itself can largely be learned given a certain base of skills, the right attitude, and a lot of reps (experience).

I was also quite impressed at Tiger's reputation to win in more than one sector (equities, commodities, currencies) as most investment funds (especially in the 1990s) weren't quite as nimble as most firms today.

Julian Robertson's reasons for ultimately closing down in 2000 is also quite prescient in today's market:

As you have heard me say on many occasions, the key to Tiger's success over the years has been a steady commitment to buying the best stocks and shorting the worst. In a rational environment, this strategy functions well. But in an irrational market, where earnings and price considerations take a back seat to mouse clicks and momentum, such logic, as we have learned, does not count for much.

The current technology, Internet and telecom craze, fueled by the performance desires of investors, money managers, and even financial buyers, is unwittingly creating a Ponzi pyramid destined for collapse. The tragedy is, however, that the only way to generate short-term performance in the current environment is to buy these stocks. That makes the process self-perpetuating until the pyramid eventually collapses under its own excess.

This NYT article from March 2001 further describes some of the reservations that he had in the internet/technology boom in 2000. A message that resonates quite well in today's market ironically.

Mr. Robertson fears for investors in companies that have little in the way of history, earnings or even revenues. ''Investors are rightly fascinated by the Internet.'' he said, ''But wrongly they do not include price in these equations. It's going to end in a real blood bath.''

Mr. Robertson was one of the last holdouts in value investing; many others have gone against their beliefs and jumped onto the technology bandwagon. ''Life and investing are long ballgames,'' Mr. Robertson said. ''The people who were cynical and jumped in and played this boom are going to win this game. But to take the cynical risk against your fundamental belief, I wonder if in the long run that will work.''

As Julian Robertson went into private investing - backing many of his employees who went on to build many of today's successful investment funds. Chase Coleman, then 25, emerged with a technology/software focus as a long-short hedge fund. Instead of focusing on North America, Chase went into markets taht historically didn't receive as much attention (especially for tech) and yet looked quite similar to their North American counterparts in terms of characteristics.

Chase also moved into the private space - making several VC investments including: Zynga (Series B), LinkedIn (via secondaries), Flipkart (Series B), Facebook (via secondaries), and Trendyol (Series B). He had a reputation of often winning deals by paying above market rate at the time, which still turned out to be a great deal in hindsight as the market has gone up since then.

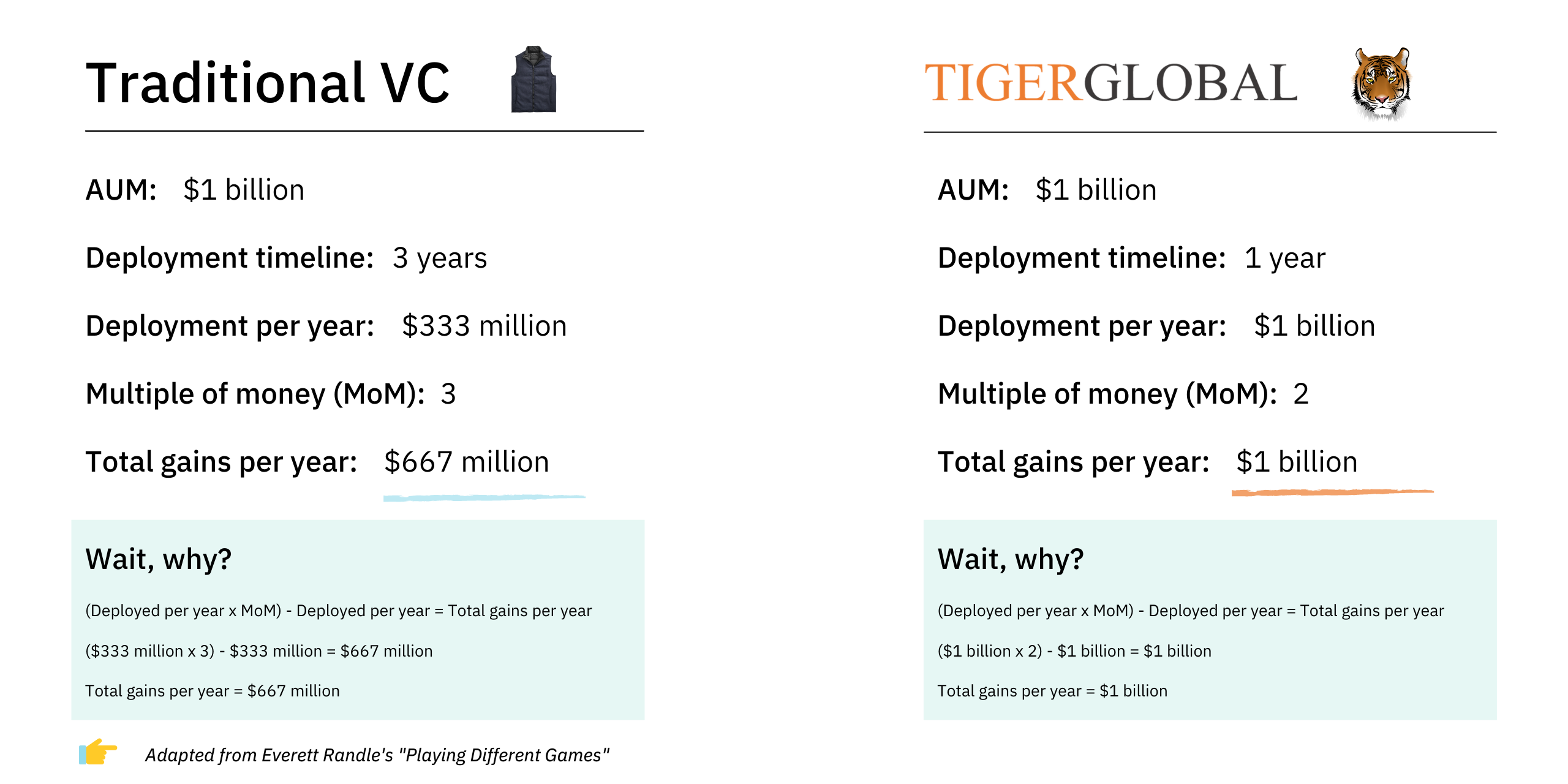

His most recent adjustment has been to deploy capital faster than most (if not all) investors. Instead of trying to differentiate from a sourcing or support perspective, Tiger Global has built a playbook to simply win more deals.

This essentially comes down to having a lower hurdle (see graphic below), casting an extremely wide net and outsourcing diligence.

Lower Hurdle

While VCs may aim to have a ~30% IRR, Tiger focuses on a lower hurdle (18%) at a faster deployment rate - creating more cash faster.

Casting a Wide Net

A key part to being able to deploy capital faster is having a much wider net vs. other investors. Given that they're willing to pay more than most/all investors, they have built a network of seed investors who are willing to show their investment to Tiger Global for a first look.

Here's an overview of their approach/criteria:

It's betting on private tech as an asset class.

It will deploy as much as $10 billion a year into this market.

It will participate at any stage, from seed to pre-IPO (and beyond).

It will invest anywhere on the planet.

This creates an incredible TAM for potential investments.

Outsourcing Diligence

The biggest reason why other firms can't match the criteria above is due to resourcing. Instead of trying to build internal teams to diligence opportunities, Tiger Global has outsourced its entire diligence to consulting firms - essentially allowing the firm to spin up 'competence' as opportunities emerge vs. making significant bets on specific sectors by building a team first.

From a deal perspective, the sheer efficiency of this model is quite remarkable. I've also seen a number of PE firms execute on roll-ups in a similar fashion. Speaking with prospective sellers, the level of inbound interest from PE firms have increased quite a bit and many have shown an ability to pay at/above market rates with the goal of closing in less than 4 weeks.

Perhaps Tiger Global has the resources to execute this strategy successfully, however it is a bit concerning when there are many other players playing a similar game despite a very different pedigree.

Here are a couple of other posts on Tiger Global that I found to be quite interesting to read:

Excess of Excesses

This is a great shareholder letter from Lux Capital that was made public, it goes well beyond a discussion around typical investment performance explains how some of our more rational investors may be thinking. It also expresses a sentiment that I have been feeling across all asset classes (real estate, public/private equities, crypto and etc).

Here are a couple of highlights from the letter:

Index-based Valuations

Valuations have risen, diligence has fallen and excess is in excess. The corrective to high prices is a heavy dose of discipline to de-emphasize auctions and re-emphasize finding founders earlier and earlier, being first-check-in partners of choice, hatching more early-stage incubations and doing more de novo company creation across all sectors. Dry powder is most valuable when liquidity, currently a flood, sloshing and abundant, turns a drought, dripping and scarce. Preparing for this turn when it comes-is wiser than predicting when it may.

For Lux, curated company creation will continue to be a unique strategy when the investment world is trending toward increasingly indiscriminate indexing of existing companies. This trend has been true in public markets, first with the shift from active to passive, and now increasingly in private markets.

Quick, Inadequate Diligence

While many investors say they won't participate in auctions where the highest price may yield an accepted term sheet-and a winner's curse-investors also must decide to opt in or out of races, where the winner is not the highest price (or just the highest price) but the quickest to move. These pacing investors-often outsourcing diligence to consultants—are observably causing other investment partnerships to laxen diligence, shorten decision cycles, and compete with term sheets with half-lives intentionally and competitively set to expire before others' regularly scheduled partner meetings.

It was common for founders to fake it before they made it, with bluffing and bluster. But in the current moment, founders' focus is preempted with pitches to them from investors of why they should take more money, open or extend rounds or do secondary transactions.

FOMO Among LPs (Investors)

Indigestion of LPs and the pace of new commitments might no longer match the pace of new raises. The supply of new funds exceeds not the demand to allocate, but the ability.

A few extreme LPs may even borrow against public holdings to make commitments lest they lose their coveted spot in a zero-sum fund (with many others eager to take their spot), taking the long view that even one underperforming fund may be a small price to pay for being in the future with a high-performing franchise.

To help combat this feeling of needing to participate in an extremely reckless investing environment while preparing for what a downturn might look like, I’ve shared a couple of tweets below that capture the importance of being patient and setting up the right boundaries so that you remain focused.

On being patient:

Setting up boundaries to create/maintain focus: